What is an Income-tax Notice?

An Income-tax Notice refers to a written correspondence by the Income Tax Department to a taxpayer regarding their tax account. These notices are dispatched for various reasons, such as failure to file Income-tax return, defect in the filed return, requesting specific information or documents, and more.

Upon receipt of a notice, it is the taxpayer's responsibility to respond within the stipulated time frame and address the issue with the tax authorities. It is important for the taxpayer to understand the notice, the requirements and the steps to comply.

How to check notices issued by Income-tax Department?

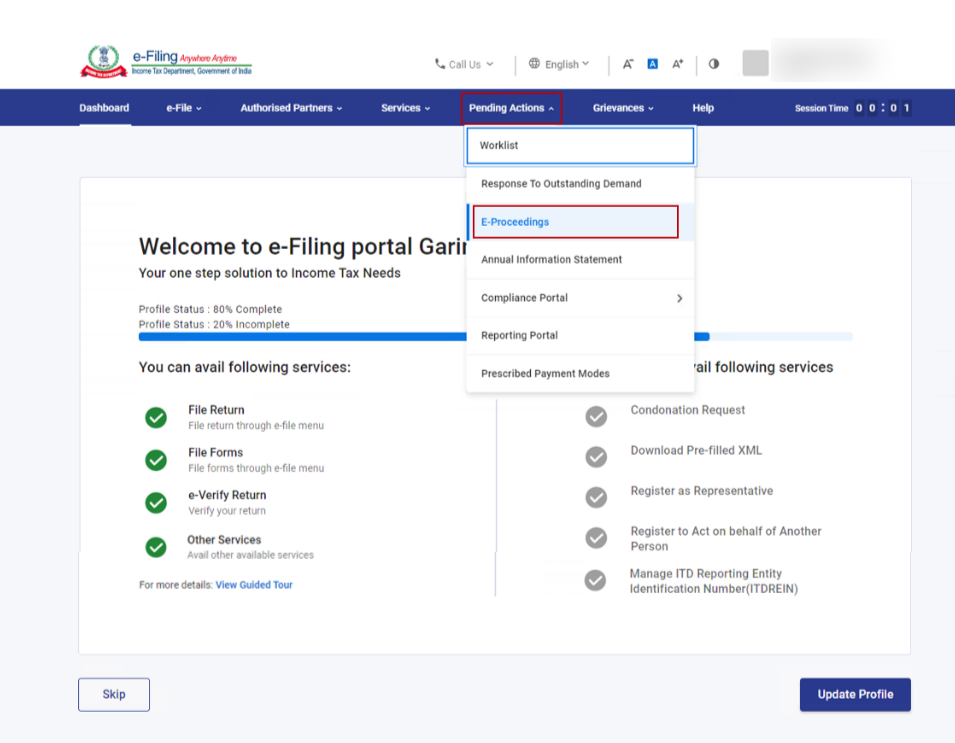

You can check if any notices have been issued to you by the Income-tax Department through the e-filing portal. Follow the steps given below to check notices issued against your PAN.

- Visit the Income-tax e-filing portal (https://www.incometax.gov.in) and login with your User ID and password.

- On your Dashboard, click Pending Actions > e-Proceedings.

- On the e-Proceedings page, click Self. This will display the list of notices issued against your PAN.

Types of Income-tax Notices

|

Type of Notice |

Description |

|

Notice under Section 139(9) - Defective Return |

This notice is issued when a filed income tax return is considered defective, and the taxpayer is required to rectify the defects within a specified period (generally 15 days). |

|

Intimation under Section 143(1) |

Once a return is filed and e-verified, the Income tax Department processes the return. The intimation under Section 143(1) is sent by the Department after processing the filed return. It provides details of the computation of total income, tax payable, and any refund due or tax demand. |

|

Notice under Section 133(6) |

This notice is issued to call for the information like investment proof, deductions proof etc. which is considered relevant or necessary for the proceedings under the Income Tax Act, 1961. |

|

Notice under Section 245 - Refund Set-off |

This notice is issued for adjusting refunds against any outstanding tax demand. |

|

Notice under Section 142(1) - Inquiry |

This is usually served to call upon documents and details from the taxpayers and to take a particular case under assessment. The basic purpose is to inquire about the details of the assessee before making the assessment under the Act. It can be related to a ‘Preliminary Investigation’ before starting the assessment. |

|

Notice under Section 143(2) - Scrutiny |

This notice is basically sent after notice u/s 142(1) has already been sent. It means the Assessing Officer was not satisfied with the produced documents or maybe the Assessing Officer has not received any documents. If you get a Notice under Section 143(2) it means your return has been selected for detailed scrutiny by your Assessing Officer. |

|

Notice under Section 148 - Income escaping assessment |

This notice is issued for reopening an assessment. It is issued if the ITD believes that income has escaped assessment and requires further investigation. |

|

Notice under Section 156 - Demand Notice |

Where any tax, interest, penalty, fine or any other sum is payable in consequence of any order passed, the Assessing Officer shall serve upon the assessee a notice of demand, specifying the sum payable. |

|

Notice under Section 131 - Inquiry and Investigation |

This notice is issued for conducting inquiries and investigations on the assessee or any related person. |

|

Notice under Section 245A |

This notice is issued for the purpose of adjusting any refund against the tax arrears or other outstanding demands of the taxpayer. |

How to respond to Income-tax Notice?

Receiving an income-tax notice doesn't necessarily imply wrongdoing. It's crucial to carefully read the notice, understand its implications, and respond within the stipulated time frame.

It is recommended to seek professional assistance if you're unsure about how to proceed.

With over 10,000 Notices resolved, myITreturn.com provides expert Notice Assistance. Our CAs and Tax Experts will review your documents and file responses for you. Click here to know more.

Comments

0 comments

Please sign in to leave a comment.